This is a brief discussion of the effect of oligopolies on an

economy. It is an example of the macroeconomic effects of microeconomic processes. The

derivation is based on the idea of the kinked demand curve, developed by Paul

Sweezy in the 1950’s.

Those not interested in the derivation may jump ahead to the

discussion at the conclusion.

Those interested may find the various derivations of kinked

demand curve theory on You Tube helpful, and perhaps easier to follow than what

I have presented here. Here’s one:

And for contrast, perfect competition:

We discuss competitive oligopolies, where collusion is not

necessary for fixed prices.

For your convenience a little background. Oligopolies are a common market

structure. Indeed, many markets seem to

evolve, or have evolved, into

oligopolies, (or its cousin, oligopsonies,)

They are ubiquitous.

An oligopoly has some of the characteristics of a monopoly,

in that its members can charge higher than normal prices and make higher than

normal profits. The particular characteristics of

an oligopoly are, 1 It consists of a

relatively few, relatively large, sellers

2. Each firm is big enough to

affect the others. 3: The products are

similar or identical. 4: There are barriers to entry, such as initial

capital costs.

The traditional analysis of oligopolies is that, rather than

a normal straight demand curve, they face a kinked demand curve D, which for a particular

firm is also their average revenue curve AR. Diagram 1 shows this demand curve for

a particular oligopolist. The

oligopolist wants to sell at the kink, which is at some price pa,

which is really determined by the market, and some quantity qa, which

is determined by other factors, which we will discuss in the conclusion.In any event, the kink is at a price higher than

the equilibrium price in perfect competition, and a quantity lower than the

equilibrium quantity. Fewer goods are produced, and consumers are forced to pay a higher price for them.

If we

were to discuss all the members of this oligopoly, they would each have a

separate, though similar, diagram. The

prices at the kink would all be the same, but the quantities at the kink might

be different.

Our oligopolist’s total revenue, that is, how much money he

takes in, is price times quantity sold, or

pa x

qa.

Why does he want to sell at price pa? If he raises his prices above pa, to

pb

hoping to make an extra profit, none of his competitors will follow. So his prices will be above theirs, and

because their products are similar to or identical to his, he will lose some,

perhaps many of his customers to them.

If his price goes up a little, the quantity of products he sells will go

way down, to qb

so he will take in less money. The area

pb

x qb, the money he takes in now, is less than the area pa x qa,

the money he took in before. This is the

characteristic of an elastic demand curve. As you move up the curve, the

quantity sold goes down faster than the price goes up.

Suppose instead he lowers his prices, below pa,

to pc, hoping to gain market share. Then his competitors will quickly follow suit,

since they don’t want to lose their market share to him. So he won’t gain market share, he’ll just be

selling at a lower price, and making less money. He may sell a few more products, at qc just

because his, and everybody’s, price is lower, but not enough to compensate for

the decrease in price. The area

pc

x qc , the money he takes in now, is less than the area pa x qa,

the money he took in before. This is the

characteristic of an inelastic demand curve.

As you go down the demand curve, the price goes down faster than the

quantity sold goes up.

Now for a firm to maximize profits, its marginal costs, MC, must equal

its marginal revenue MR. This is always the case, but what does this

mean? Marginal cost is the increase in

total cost accrued by the firm for the next unit it produces. If the firm produces 4 units for $60 and 5

units for $90, then the marginal cost of the fifth unit is $30.

Marginal revenue is the increase in revenue that results

from selling one more unit. For

imperfect competition, as we have in the case of oligopolies, MR is always

less than the average revenue, AR. This is because when you sell more units, you

have to sell them at a lower price, but you have to sell all your units at that lower price.

So if you sell 4 units at $100 total revenue and 5 units at $120 total

revenue the average revenue AR,

the price you are selling them at, for 5 units is $24, but the marginal revenue

MR for

the 5th unit is only $20.

Profit is maximized when MR

= MC because when MC

is greater than MR,

it costs more to produce the next unit than you get paid for it. With the figures we used, you would produce 4

units for $60, sell them for $100, and make $40 profit. If you were maximizing profit, you wouldn’t

make 5 units for $90, having to sell them at $120, and only make $30 profit.

See Diagram

2. The marginal cost MC curve is the

lopsided “u.”

When you produce something, costs first go down, savings of scale, then they go

up, dissavings of scale. (Imagine a

restaurant. The first meal is very

costly, because of all your fixed costs. As you produce more, each next meal is

cheaper to produce, as you use your assets more efficiently, until you reach

some minimum. Then the costs per each

additional meal start going back up, because you run out of stove space, people

start getting in each others way, etc.)

With the kinked demand or AR

curve, the MR

curve is very strange. The upper ARU and the upper MRU curve, the curves

above the kink, both start at the same

point on the axis, (in the direction where the arrows come together,) but the MRU curve descends more steeply, twice as steep, it

turns out. When they reach the kink, however, the MRL

and ARL curves, the curves

below the kink, also extend from a point on the axis, (much higher on the axis)

in the direction of the dotted arrows, so the MRL curve, being twice

as steep as the ARL curve, is much lower than the MRU curve at the kink. In this

diagram, in fact, it is so much lower it is negative, which means MRL curve is irrelevant. What is not irrelevant is the fact that,

because MRL is negative, the MR curve which

connects the MRU and MRL curves, (green line) crosses the Q axis at the kink. This means that the quantity of production of

maximum revenue (which is where the MR

curve crosses the Q

axis) and profit maximization (where MR

= MC)are at the same quantity, qa.

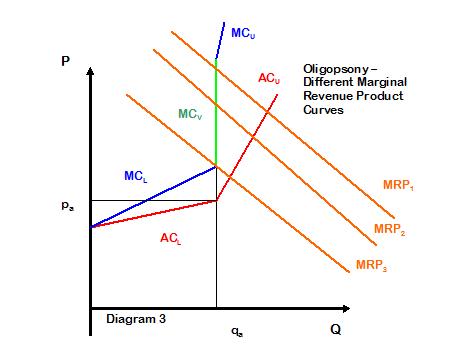

What is important is the green line, the MR curve at the

kink. Now since, when we maximize

profit, MR

= MC, when ever MC

crosses the green line, the profit maximizing quantity and price are

going to stay the same. See Diagram 3. The firm, whether its marginal cost curve is MC1, or MC2 or MC3 is going

to want to produce the same amount, and charge the same price. Here this will maximize both profit and

revenue.

Conclusion:

Even in competition, oligopolists can make

extra-normal profits. Firms in

oligopolistic competition tend to be locked in to price, so they must find

other ways to compete, and maintain or gain market share. (We make the casual observation that one need

look no further than oligopoly pricing (and as we shall see, oligopsony

pricing) to deduce a cause for Keynesian ‘price stickiness.’ In an economy rife with oligopoly we would

expect many points of price, and quantity, fixedness, making deflation a uneven

and problematic process.) The owner of a

service station, for instance, locked in competition with 3 other service

stations at an intersection, might, to attract more customers, initiate full

service, or add a convenience store or coffee shop. He might do this, raising his costs, until

the marginal cost curve was something like MC3 in Diagram 3. The oligopolist would not want to

raise costs any more, because then his profit maximization would occur at a

price higher than pa, and he

would lose market share.

However, the opposite can also happen. Since price is, with in a range, independent

of costs, the oligopolist may decide to shave costs, cut corners, and so

increase his profit that way. Were an

industry to do this, we would have a situation like the American auto industry

in the 60’s and 70’s, before imports began to significantly impact on their

market.

Oligopolies do not consist of identical or identically sized

firms, with identical shares of the market. The quantity a particular oligopolist

sells at is determined by historical factors, and his ability, or inclination,

to compete in ways which do not affect the price. Historical factors, for instance, most

notably their activities during the period their industry was more competitive

and open, determined the relative sizes of GM, Ford, Chrysler, and American

Motors, back when they constituted an oligopoly. Foreign Competition and decisions since have

changed their relative sizes and profitability.

Another point is that, unlike perfect competition, firms of

various efficiencies can co-exist in an oligopoly, operating at differing

capacities and different economies of scale, each firm collecting its

particular degree of profit. And unlike

perfect competition, much of this profit is extra-normal, more than the profits

we would expect to see from perfect competition, which tends to drive profit to

a minimum.

What other things might we expect? Well, we would expect the transfer of some

consumer surplus to the producer, in the form of his extra-normal profits. Consider that oligopolies are becoming

economically pervasive. Each of these oligopolies

extracts its rent, transferring resources from consumers, to the oligopolists. Indeed, to simplify considerations, let us

just model the entire economy as two tiers, consisting of an oligopoly and its

market. Consider first perfect

competition, where the economy was efficient and in balance, Diagram 4.

Supply equals demand and the equilibrium point is at e, and surplus

is divided between consumer and producer. (Consumer’s Surplus is

exaggerated a bit, to keep the lines the same. Sorry.)

With oligopoly, Diagram

5, there is a net transfer of surplus from the consumer to the

oligopolists. (the greenish-yellow box)

In the real economy, this would be manifest as higher

corporate profits, and, since most corporate stock is held by the wealthy, an

increase in income of the wealthy.

Corresponding to this, we would expect a decrease in the welfare of the

rest of the economy, as the increase in income of the wealthy has to come from

somewhere.

Efficiency has also declined because an oligopoly produces

less than the competitive equilibrium production, at a higher price creating

deadweight loss: The blue triangle. That is, the economy is producing less than it

would otherwise, less than consumers would be willing to buy at the lower,

equilibrium, price. Indeed, the economy

may perhaps be producing less than it needs to.

For instance, since the public sector is also supplied by the private

sector, as the private sector becomes increasingly organized as oligopoly, we

would expect public sector costs to increase disproportionately. We would also expect, due to dead weight loss,

an increasing shortage, and/or a decline of the quality, of public goods. This includes much of the infrastructure the

private sector, the oligopolist, relies on.